Reduce Your Credit Card Debt By Up To Half

See how much you can save with a free, no obligation consultation.

Reduce Your Credit Card Debt By Up To Half

Save thousands by lowering your debt balance and wiping away years of future interest and payments.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

Company Name

"renowned for its client-centric approach"

"offers a crucial lifeline"

"a new standard in debt relief"

"enhancing the effectiveness of debt relief strategies"

"tangible, quick results"

Breaking Free From Credit Card Debt Can Feel Overwhelming

When you don't have a plan...

- Your stress level spikes each month

when your bills are due

- You can only afford to make the minimum payments on your credit cards

- Your high interest debt balance grows

faster than you can keep up with

Are you tired of sleepless nights full of stress and constantly feeling overwhelmed? We're here to offer a better way. Pacific Debt Relief has helped thousands of people just like you become debt free faster, for significantly less than they owe.

Don't waste another day worrying about your debt, see how quickly you could be debt-free today.

How Does Our 3-Step Program Work?

You stay in control, we do the work for you.

1. Free, No Obligation

Debt Consultation

Talk to our Certified Debt Specialist to assess your financial situation and see if you qualify to have up to half of your debt balance reduced. It only takes a few minutes to find out exactly how much you could save.

2. We Negotiate Your

Debt Down

Once enrolled, we create an affordable, personalized plan for you to become debt free. Our negotiators work with your creditors directly to reduce your debt balance. This saves you time and lets you focus on what matters.

3. Your Debt Balance

Decreases

We repeat this process for each creditor until all your accounts are settled for a reduced amount. You'll be debt-free much faster than you ever thought possible.

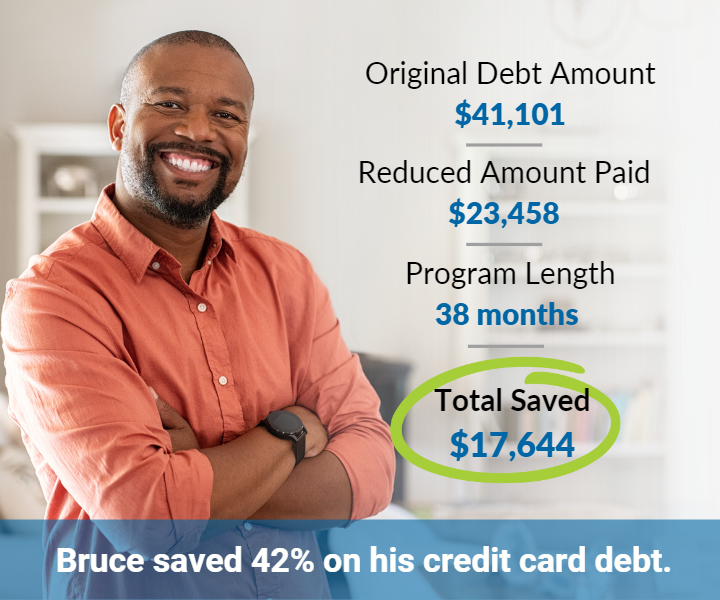

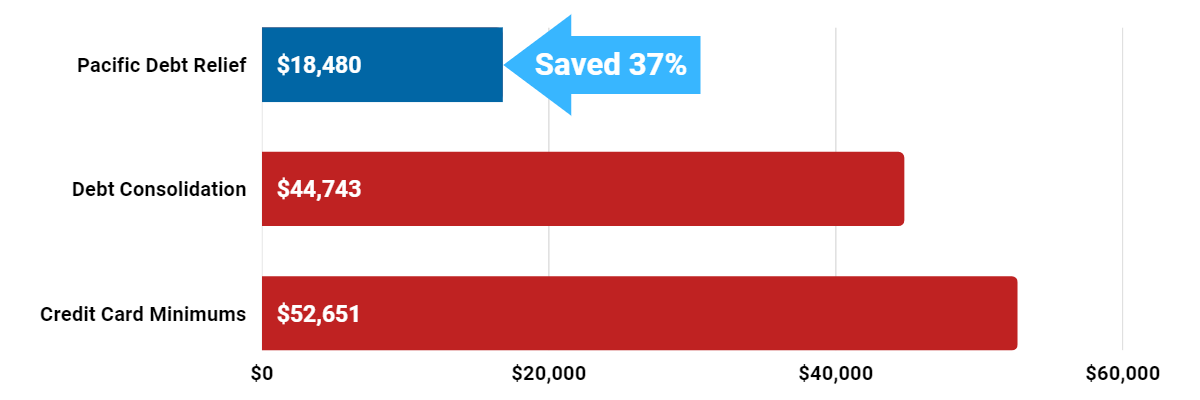

Pacific Debt Relief offers the only solution that significantly reduces your debt to less than you currently owe. That means you get debt-free in a fraction of the time it would take with any other option.

The Only Option That Reduces Your Debt Balance

Nathan owed $29,381 in credit card debt.

Here's how much he paid (and saved!) through our program, and a comparison of what he would have paid through other debt relief options.

Types Of Debt We Help With

- Credit Cards

- Personal Loans

- Lines of Credit

- Medical Bills

- Store Cards

- Collections

- Repossessions

- Business Debts

With You Every Step Of The Way

From your first phone call with us to the moment you become debt-free, our team is here to partner alongside you.

Hear how Pacific Debt Relief helped Suzanne reduce her debt, and get her back on track to a happier, healthier financial future.

Worry-Free Debt Relief

A Plan That Fits

Your Budget

Our program puts you in control, which means you choose the debt-free plan that best fits your budget. And since most of our plans have payments that are considerably less than your typical credit card minimums, you'll have more money left in your bank account each month.

With You Every Step Of The Way

Our account team is here to ensure that things run smoothly, so you can focus elsewhere. Once you enroll, you'll have a dedicated Account Manager who will help guide you throughout the program.

Top Rated Customer Service

Consistently ranked "Best Debt Settlement Company" for customer service. We value your time and are dedicated to being your partner through the process of becoming debt free.

What Customers Say About Us

20 Years of Dedicated Service

We are celebrating 20 years of excellent customer service and support to our clients at Pacific Debt Relief. We are honored to have provided debt relief services to our communities and helped support our customers in becoming financially free over the past 20 years.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

Company Name

"renowned for its client-centric approach"

"offers a crucial lifeline"

"a new standard in debt relief"

"enhancing the effectiveness of debt relief strategies"

"tangible, quick results"

Save

Up To Half

Reduce your credit card balance by up to half and consolidate your debt into a single, affordable payment.

Get Debt-Free

Faster

Get debt free up to 5X faster, saving you years of future interest and debt payments.

A+

BBB Rating

We are trusted by thousands to help lower their debt and relieve their financial burden.

Over 20 Years

in Business

Have peace of mind knowing that Pacific Debt Relief has been helping people just like you become debt free for over 20 years.

Feeling overwhelmed by credit card bills and high interest debt?

Common Signs of Financial Stress:

- You feel anxiety each month when your bills are due

- You struggle to make the minimum payments on your credit cards

- Your high interest debt balance is growing faster than you can keep up with

Discover our 3-step plan to become debt-free and don't waste another day worrying about your debt.

Start today.

How Does Our 3-Step Debt-Free Program Work?

You stay in control, we do the work for you.

1

Get a Free, No Obligation Debt Consultation.

Talk to our Certified Debt Specialist to assess your financial situation and see if you qualify to have up to half of your debt balance reduced. It only takes a few minutes to find out exactly how much you could save.

2

We Negotiate Your Debt (Way) Down.

We create an affordable, tailored plan for you to become debt-free. Our negotiators work with your creditors directly to reduce your debt balance, saving you years of future interest and debt payments, so you can focus on the things that matter to you.

3

You Save - and Become Debt Free Faster.

We repeat this process for each creditor until all your accounts are settled for a significantly reduced amount. You'll not only save more with low payments each month, you'll be debt-free much faster than you ever thought possible.

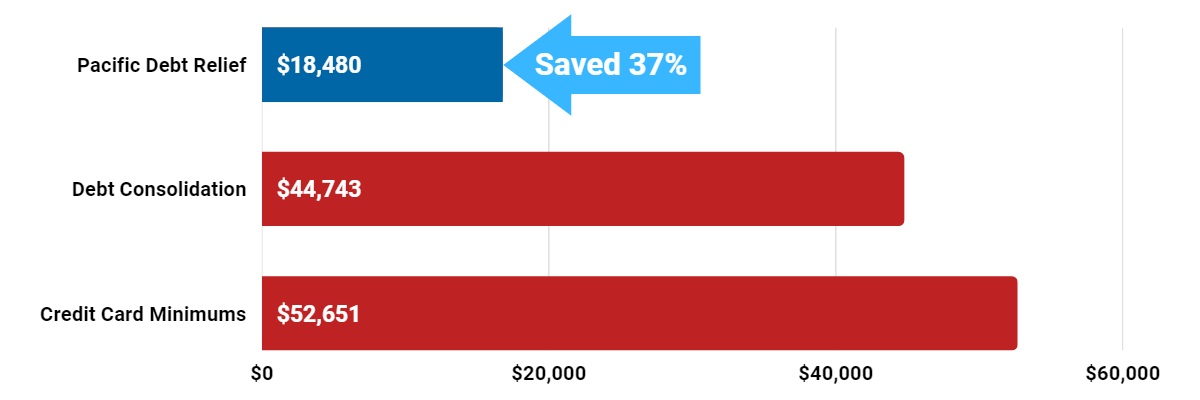

Pacific Debt Relief offers the only solution that significantly reduces your debt to less than you currently owe. That means you get debt-free in a fraction of the time it would take with any other option.

The Only Option That Reduces Your Debt Balance

Nathan owed $29,381 in credit card debt.

Here's how much he paid (and saved!) through our program, and a comparison of what he would have paid through other debt relief options.

Pacific Debt Relief offers the only solution that significantly reduces your debt to less than you currently owe. That means you get debt-free in a fraction of the time it would take with other options.

Nathan owed

$29,381 in credit card debt.

Here's how much he paid (and saved!) through our program, and a comparison of what he would have paid through other debt relief options.

The Only Option That Reduces Your Debt Balance.

Types Of Debt We Help With

- Credit Cards

- Personal Loans

- Lines of Credit

- Medical Bills

- Store Cards

- Collections

- Repossessions

- Business Debts

Why People Believe In Us

BBB Reviews | 4.9/5.0 Rating

Leticia M.

"I clearly understood all programs available and the details to make the correct decision for my situation. [Pacific Debt Relief] was very understanding, patient, and professional. I'm glad I decided to go this route. Finally peace of mind."

Bailey O.

"[Pacific Debt Relief] was extremely professional while still being relatable and making me feel like my problems and struggles mattered without making me feel horrible or embarrassed by my situation. I'm extremely grateful to finally have a solution after 5 years of struggling."

Kari D.

"The last 3 years have been a set of one set back after another. I felt sick in the stomach everyday. Horrible about not being able to get ahead with anything. I felt like I was slowly drowning. Pacific Debt helped me so much and never once made me feel like I was a horrible person for falling so far behind! Thank you, you saved my financial and mental life with a piece of mind someone legitimate was helping me."

Paul L.

"The agent I spoke to was very understanding and thorough in the process I was about to embark on. I am now at ease and looking forward to reducing my credit card debt. Thank you for the outstanding service!"

With You Every Step Of The Way

From your first phone call with us to the moment you become debt-free, our team is here to partner alongside you.

Learn how Pacific Debt Relief helped Suzanne reduce her debt, and get her back on track to a happier, healthier financial future.

20 Years of Dedicated Service

We are celebrating 20 years of excellent customer service and support to our clients at Pacific Debt Relief. We are honored to have provided debt relief services to our communities and helped support our customers in becoming financially free over the past 20 years.

Frequently Asked Questions

-

Why should I trust Pacific Debt Relief?

For over 20 years our debt relief program has helped clients change the trajectory of their financial lives. Our work has impacted families and future generations. We are a nationwwide debt settlement company that provides excellent customer service and works diligently to maintain your trust throughout our entire process.

Don't just take our word for it, read our third-party reviews by visiting our Pacific Debt Relief reviews page or our video testimonials. We're rated A+ and fully accredited by the Better Business Bureau (BBB). We have thousands of reviews and testimonials highlighting we are trustworthy, we keep our word, we have a friendly dedicated customer care team, we offer tailored programs to suit your unique needs, and offer ongoing encouragement throughout the process of becoming debt free. We also provide practical personal finance tips and strategies through our financial educational resources to help you better manage your money and debt.

During your Free Consultation we will listen closely to your financial situation and create a tailored program to get you debt free faster than you thought possible. We are ready to help you! Call us today.

-

How do I qualify for Pacific Debt's debt relief program?

To be qualified for our debt relief program, you must have more than $10,000 in unsecured debt (credit card debt, payday loans, personal loans, medical bills, collections and repossessions, business debts, and some student loans).

We cannot help with debt from lawsuits or judgments, IRS debt, utility bills, auto or governmental loans, mortgages or home loans, or other secured debt.

-

Can Pacific Debt Relief really help me?

Are you feeling the weight of your debt? Are your past financial choices impacting your future? We're here to offer a better way. For the past 20 years we have settled over $500 million in debt for our consumers. Call us today to hear how we could provide you with a customized financial plan to cut your monthly payments immediately giving you the cash flow and peace of mind you need.

Pacific Debt Relief is a nationwide debt settlement company recognized by numerous independent consumer review companies, including the Better Business Bureau. We have helped thousands of people reduce their debt, and we can help you too! Give one of our certified debt relief counselors a call to understand your options. You can also enroll in our debt settlement program.

-

What is Pacific Debt Relief's program?

Our nationwide debt settlement program is comprehensive and keeps you in control. Once you make the decision to get out of debt, you apply through our website. You’ll be connected with a certified credit counselor who will review your debt relief options with you. If debt settlement is right for you, we move forward with enrolling you into our debt relief program.

Our debt relief program is quick and painless!

Step 1 – Enroll through the Pacific Debt website

Step 2 – Our Client Care department will guide you and give you a clear understanding of how our debt relief program works

Step 3 – Sit back and let our professional debt negotiation team work for you and start saving you money!

As you enter the debt settlement process, your assigned certified debt relief counselor will analyze your debt, monthly expenses, and your income. They look at your current budget and determine a payment estimate that works for you. Once enrolled, our negotiation team will work with your creditors to agree on a (usually) lesser amount of debt and a repayment schedule.

Debt settlement includes unsecured debt such as medical bills, overdue utility payments, credit cards, personal loans, tax debt, payday loans, bankruptcy, and certain contracts, like gym memberships. We have trusted partners who will help you with payday loans and student loan consolidation.

-

What areas does Pacific Debt Relief service?

Pacific Debt Relief is a nationwide debt settlement company. Below are the states we service.

Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, District of Columbia, Florida, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Maryland, Massachusetts, Michigan, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, New York, North Carolina, North Dakota, Ohio, Oklahoma, Pennsylvania, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Vermont, Washington, West Virginia, Wisconsin, Wyoming

-

I'm thinking bankruptcy, is it right for me?

People often talk about bankruptcy and how you can declare bankruptcy to get out of debt. In reality, bankruptcy is a last resort. Keep in mind these points:

- Bankruptcy can be very expensive, largely due to the legal fees

- Bankruptcy has a stigma attached to it

- Bankruptcy details are a public record

- Bankruptcy can stay on your credit report up to 10 years

- Loans after bankruptcy can be very expensive and difficult to obtain

At Pacific Debt, we only recommend bankruptcy as the last possible resort. There are several other debt-relief options to try first. These include:

- Debt Settlement – working with your creditors to agree on a lower amount to repay

- Debt Consolidation – rolling all your debt into a lump sum and paying it off entirely

- Debt Consolidation Loans – getting a loan to pay off all the debt, then repaying the loan at a better interest rate

- Credit Counseling Services – assistance with budgeting and negotiating lower interest rates

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

Company Name

Worry-Free Debt Relief

A Plan That Fits

Your Budget

Our program puts you in control, which means you choose the debt-free plan that best fits your budget. And since most of our plans have payments that are considerably less than your typical credit card minimums, you'll have more money left in your bank account each month.

With You Every Step Of The Way

Once you enroll, you'll be supported by our dedicated Client Success team, who will help guide you throughout the program.

Top Rated Customer Service

Consistently ranked "Best Debt Settlement Company" for customer service. We value your time and are dedicated to being your partner through the process of becoming debt free.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

This is a paragraph. Writing in paragraphs lets visitors find what they are looking for quickly and easily.

Company Name

Do Not Sell My Personal Information

Do Not Sell My Personal Information