Get in touch

(833) 865-2028

inquiries@pacificdebt.com

Alabama Debt Relief

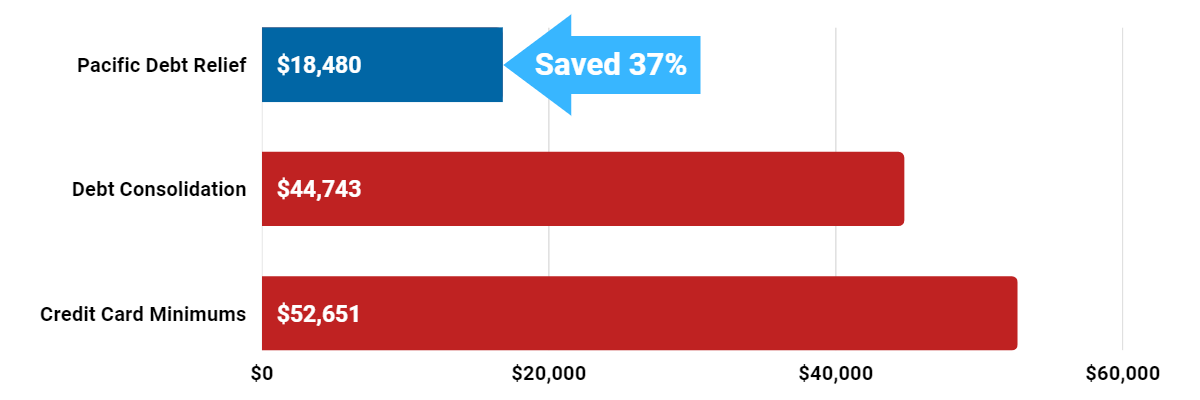

Reduce Your Credit Card Debt By Up To Half

Pacific Debt Relief offers the only solution that significantly reduces your debt to less than you currently owe. That means you get debt-free in a fraction of the time it would take with other options.

Save thousands by lowering your debt balance and wiping away years of future interest and payments. Call today for a FREE consultation!

What are Alabama Debt Relief Programs?

Alabama debt relief involves debt reduction through debt settlement or debt consolidation.

Pacific Debt Relief specializes in debt settlement. We work to reduce your debt for less than you owe. Most unsecured debt qualify for the Pacific Debt relief program, including credit card debts. Pacific Debt deals directly with your creditors including credit card companies while guiding you throughout the entire process.

Our best-rated settlement programs are available for Alabama residents. Call our certified specialists who will explain all your relief options. Our free debt analysis will help you make an informed decision about your unsecured debts. Call to get your free quote for our debt settlement services.

How Does Debt Relief Work?

Debt relief reduces the amount you owe your creditors so that you can receive relief for your personal finance situation. Debt settlement is one option. Pacific Debt provides relief in the form of debt settlement to Alabama residents, as well as nationally.

The first step for Alabama residents in finding relief is a FREE phone call with one of our debt specialists who can lay out all your options, so you understand your position and what steps need to be taken in order to reduce your debt.

Is Alabama Debt Relief Legit?

Pacific Debt has helped countless Alabama residents reduce their debt and live debt free. Since 2002, we've settled over $300 million in credit card debt for our clients.

Contact us today to see how we can help.

Alabama residents searching for information on debt consolidation or for a debt management plan may benefit from a free conversation with our debt specialists.

We may be able to help lower your monthly payments or even become debt-free. If you are looking for consolidation loans but have bad credit, our debt settlement program might be perfect for you!

We are experts at debt negotiation so call for your financial situation. We do not require a personal loan. Instead we negotiate to reduce interest rates, offer helpful resources, and a low total monthly payment with no upfront fees.

During Pacific Debt's program, you deposit an agreed single monthly payment amount in your own escrow bank account. As you build up sufficient funds, we pay your settled accounts.

Take time to understand how debt settlement programs work and all your Alabama relief options.

What to expect from our Alabama Debt Settlement Services

- Affordable monthly payment based on your budget

- Resolve your situation in 2-4 years

- No upfront fees with low monthly fees that vary from 15-25% of the total enrolled amount and state of registration

- Personal attention from your assigned Account Manager and Certified Debt Specialist

- Repayment plan and possibly lower interest rates.

- Excellent Customer Service & Support

- We negotiate decreased balances and lower interest rates

Who qualifies for debt settlement?

You must meet the following to be eligible for our debt relief program:

- Outstanding balances of at least $10,000 in unsecured debts (credit card bills, payday loans, personal loans, doctor bills, collections and repossessions, business debts, and some student loans).

- Difficulty making minimum payments

- Live in Alabama, Alaska, Arizona, Arkansas, California, Colorado, District of Columbia, Florida, Idaho, Indiana, Kentucky, Louisiana, Massachusetts, Maryland, Michigan, Minnesota, Missouri, Mississippi, Montana, North Carolina, Nebraska, New Mexico, New York, Oklahoma, Pennsylvania, South Dakota, Texas, Utah, Virginia, or Wisconsin

* Since not all states are included, not all clients can enroll in our company. People in other states can be connected to one of our trusted partners

There are some tax consequences to debt settlement as debt forgiven is considered income. Before pursuing debt settlement, discuss potential tax consequences with a tax professional.

We are also not a law firm and are not giving legal advice.

Pacific Debt Relief Accreditation

We are accredited by:

- The Consumer Debt Relief Initiative

- International Association of Professional Debt Arbitrators

- Better Business Bureau

Alabama Debt Relief Reviews

Alabama Better Business Bureau

Pacific Debt Relief is an A+ rated business with the BBB. We have been accredited since 2010. We have received 4.87 out of five stars based on 40 customer reviews with the BBB.

Alabama Debt Relief Help

Click here to get your FREE Consultation & Savings Estimate , or call us at 800-909-9893.

We can help Alabama residents throughout the state, including Birmingham, Montgomery, and other cities. We can help you and your family with relief from debt in the state of Alabama, or even nationwide.

State of Alabama

Alabama is home to the Gulf shore to the foothills of the Appalachians. Forestry and agriculture were the backbones of the state's economy, but recent years have seen increases in aerospace, healthcare, banking, and automobile manufacturing. Alabama is ranked #24 for population and #27 for population density.

As of 2018, over 10 million people called Alabama home. Birmingham is the largest city in Alabama.

Alabama Income

The median state income is $46,257. As of 2018, the minimum wage is $7.25 per hour. Unfortunately, 24.3% of Alabamian children under 18 live in poverty. For residents overall, 17.1% of all people in Alabama live under the poverty level.

- Median state income: $46,257

- Minimum wage: $7.25/hour

- Children in poverty: 24.3%

- People in poverty: 17.1%

Is Alabama a Community Property State?

Alabama is not a community property state. Therefore your assets are not seen as equally owned by you and your spouse. Currently, there are only 9 states including Louisiana, Arizona, California, Texas, Washington, Idaho, Nevada, New Mexico, and Wisconsin that are community property states. In the state of Alabama, the judge will decide which assets are shared by you and your spouse, and what the equity is for each.

Homeowners in Alabama

More than half (70%) of Alabamians hold a mortgage. The median home price in Alabama is $126,800 (2018). Of course, that median price depends on the location with some areas being much higher.

- Homeowner rate: 70%

- Median home price: $126,800

Alabama Employment

Alabama's current unemployment rate is 3.8%. However, the underemployment rate is 10.4%. Underemployment is the percentage of civilian workers who are unemployed, employed part-time or are not seeking employment.

If this is you, we can help. Pacific Debt offers Alabama debt relief solutions tailored to your unique situation and budget. Our certified counselors help you work up a budget and explain your options.

- Unemployment: 3.8% (2018)

- Underemployment: 10.4% (2017)

Alabama Debt

Alabamians carry a lot of debt. The average credit card debt is $7,105 (2018). The average student loan debt is $31,257. When you add all that debt on top of the cost of homes (rental or owned), versus the median income, it is very easy for Alabamians to get into debt.

- Avg credit card debt: $7,105 (2018)

- Avg mortgage debt: $140,963 (2017)

- Avg student loan debt: $31,257 (2017)

Alabama Statute of Limitations

Alabama's statute of limitations lays out maximum time periods that debt collectors can take action against a delinquent debt. These statutes of limitations begin on the date that your debt goes delinquent.

For debts taken out in Alabama, the following are the statutes of limitations for different types of debt.

- Oral agreements: 6 years

- Written contracts: 6-10 years

- Promissory notes: 6 years

- Credit cards and other revolving loans: 3-6 years

Alabama Debt Relief Programs

If you have more debt than you can pay off, Pacific Debt can help you consolidate your debt and learn to live debt free. Since 2002, we've settled over $300 million in debt for thousands of clients. We are a nationally top ranked debt relief company located in San Diego.

We will help you work through our proven and comprehensive debt relief programs. Your certified debt relief counselor will review all your options. If debt settlement is right for you, we move forward with our debt relief programs and work to save you money. Pacific Debt can help with most unsecured debt like credit card accounts, personal loans, medical bills, and repossessions.

Pacific Debt, Inc

We are one of the nationally top-ranked debt settlement companies and we have helped countless Alabama residents with our national program. Contact our professional debt negotiators today so we can help you too!

Call us and ask our award-winning debt specialists about our settlement program and how it can help you reduce debt faster.

Alabama Debt Relief Programs

We are a debt settlement company and have discussed debt settlement in detail. Click here to learn more about debt settlement. Debt settlement can temporarily harm your credit report.

We want you to understand your options including debt consolidation, credit counseling, and bankruptcy.

Read all program materials prior to enrolling with any program.

Alabama Debt Consolidation program

This rolls all debt into a low interest rate debt consolidation loan, often home equity loans, or work with a company to set up a consolidation plan. You may want to speak with someone about debt management programs.

Click here to learn more about debt consolidation and debt consolidation loans.

Alabama Credit Counseling

redit counseling helps you learn money management including developing a budget, helping you understand your credit score, and set up a debt management program. This debt management program does not involve any settlement or reduction in interest rates.

Look for professional credit counselors from a non-profit credit counseling organization.

Click here to learn more about Credit Counseling.

File Bankruptcy

Filing bankruptcy is a last resort option – this legal action wipes out most of your total debt, severely damages your credit with a credit reporting agency for up to ten years, and is expensive and time-consuming.

Click here to learn more about bankruptcy.

Avoid credit repair services as there is nothing they can do that you cannot do for yourself to improve your credit report.

Contact Pacific Debt for a free debt evaluation today so we can help you with your creditors.

Debt Collection Laws

Alabamians are protected against unscrupulous debt collectors. The federal Fair Debt Collection Practices Act (FDCPA) prohibits debt collectors from using abusive or harassing bill collection practices. In addition, the Alabama Fair Debt Collection Practices Act (AFDCPA) adds protections against more types of collectors and actions. If you are a victim of any of these actions, you may take legal action against them.

Overall, debt collectors can NOT:

- Charges more than 10% interest

- Garnish more than 25% of wages

- U se/threaten physical force or criminal tactics to harm you, your property, or your reputation

- Accusing you of committing a crime for not paying the debt

- Make/threaten to make defamatory statements to someone else

- Threaten arrest, to seize assets, or garnish wages unless actually planning to take such action

- Use obscene or profane language

- Cause you to spend money you wouldn’t otherwise have spent (ie long-distance telephone calls)

- Call you repeatedly or let your phone ring repeatedly

- Call frequently

- Contact your employer, except to verify employment or health insurance status, garnish wages or locate you

- Reveal information about debt to anyone except your spouse or your parents if a minor.

- Publicly publish your name for failing to pay

- Send a postcard or letter with revealing information on the envelope

- Claim to be someone other than a debt collector, including a governmental official

- Use stationery that appears to be from a law firm

- Charge you collection or attorney’s fees unless legally allowable

- Threaten to report you to a credit reporting agency if they have no intention of doing so

- Send a letter claiming to come from a claim, credit, audit, or legal department unless it actually is

Debt collectors must:

- Disclose caller identification

- May contact your family to locate you

- Must serve you with notice of a lawsuit if suing you

Alabama Bankruptcy Court Information

Bankruptcy is a legal action that can erase most of your debt as well as your credit history. It is not an action to take lightly. If you do, you must follow the following steps in Alabama.

Persons filing for bankruptcy must:

- Complete credit counseling within six months before filing for bankruptcy.

- Complete a financial management instructional course after filing bankruptcy.

- Complete a Bankruptcy Act Means Test to determine if you are eligible for a Chapter 7 or 13 bankruptcy

- Itemize current income sources; major financial transactions; monthly living expenses; debts (secured and unsecured); and property (all assets and possessions, not just real estate).

- Collect last 2 years of tax returns, deeds to real estate you own, car titles, and loan documents

- File for bankruptcy

- Chapter 7 bankruptcy fee is $306

- Chapter 13 bankruptcy fee is $281

- Meet with court assigned bankruptcy trustee

- Attend a Meeting of Creditors

- Confirm plan if filing for Chapter 13 bankruptcy

DISCLAIMER: We are not lawyers and are not giving legal advice. Before filing bankruptcy, talk to a lawyer in your state. The information included on this site is for educational purposes only. Your state may not qualify for the Pacific Debt, Inc debt relief program. If it does not qualify, we can refer you to a Trusted Partner or assist in connecting you with a provider who offers servicing in your state of residence.

Pacific Debt Relief

750 B Street Suite 1700

San Diego, CA 92101

Hours of Operation

Mon-Thurs: 6am - 7pm PST

Friday: 6am - 4:30pm PST

Saturday: 7:30am - 4:30pm PST

Clients

Phone: (877) 722-3328

Fax: (619) 238-6709

Email: cs@pacificdebt.com

Non-Clients

Phone:

Fax: (619) 238-6709

Email: inquiries@pacificdebt.com

"Subscribe, follow, like, share, let's get social..."

"To eliminate debt one household at a time, while placing people first." - Pacific Debt

© 2024 Pacific Debt Inc. dba Pacific Debt Relief, all rights reserved.

California Privacy Policy |  Do Not Sell My Personal Information

Do Not Sell My Personal Information

GLBA Privacy Notice | CDRI Accredited Member

*We do not discriminate on the basis of race, color, religion, sex, marital status, national origin or ancestry.

*Please note that all calls with the company may be recorded or monitored for quality assurance and training purposes.

*Your visit to our website may be monitored and recorded from essential 3rd party scripts.

*Clients who make all their monthly program deposits pay approximately 50% of their enrolled balance before fees, or 65% to 85% including fees, over 24 to 48 months (some programs lengths can go higher). Not all clients are able to complete our program for various reasons, including their ability to save sufficient funds. Our estimates are based on prior results, which will vary depending on your specific circumstances. We do not guarantee that your debts will be resolved for a specific amount or percentage or within a specific period of time. We do not assume your debts, make monthly payments to creditors or provide tax, bankruptcy, accounting or legal advice or credit repair services. Pacific Debt is not a credit repair firm nor do we offer credit repair services. Our service is not available in all states and our fees may vary from state to state. Please contact a tax professional to discuss potential tax consequences of less than full balance debt resolution. Read and understand all program materials prior to enrollment. The use of debt settlement services will likely adversely affect your creditworthiness, may result in you being subject to collections or being sued by creditors or collectors and may increase the outstanding balances of your enrolled accounts due to the accrual of fees and interest. However, negotiated settlements we obtain on your behalf resolve the entire account, including all accrued fees and interest. C.P.D. Reg. No. T.S. 12-03825.