Get in touch

(833) 865-2028

inquiries@pacificdebt.com

Rated One of The Best Debt Settlement Companies

Pacific Debt is an accredited member of the Better Business Bureau, stands among the best debt relief companies in the industry. Our exceptional service, backed by years of experience with debt settlement, has led to recognition from numerous consumer review platforms, making us a trusted choice for debt relief.

We specialize in reducing unsecured debt with proven results. Since getting help with paying off debt is a difficult decision, our system is set up to help you feel comfortable and to understand what is happening with your case every step of the way.

Contact us today for a FREE consultation with no obligation. We can help you understand all your debt relief options.

What makes Pacific Debt Relief great?

- Full accreditation with the International Association of Professional Debt Arbitrators, the Better Business Bureau and CDRI

- Long term success with debt settlement

- Award winning debt specialists

- Licensed and bonded

- Longevity of business - since 2002

Our accreditation demonstrates our commitment to excellence. Among our many awards and certifications, Pacific Debt Relief earned a BBB Accredited rating. Our track record speaks for itself. We have settled over $300 million in debt for our clients since 2002. While our accreditation speak to the seriousness of our commitment to you, check out what real clients have to say about Pacific Debt, Inc.

Pacific Debt, Inc offers award winning customer service. Our debt specialists help people understand their debt solutions and debt relief options because not one solution will fit every situation. Our debt specialists make sure you feel comfortable discussing what the best route of action is for your personal situation, whether it be payday loans, credit card debt, personal loans, or any other unsecured loan debt.

Check out the reviews below or verified sites like Trustpilot for real comments. We are very proud that our clients give us excellent ratings and we strive to keep our rating high through excellent customer service and results.

What Our Debt Consolidation Customers Say

Who is the Best Debt Consolidation Company?

Pacific Debt has been ranked as "One of the best debt settlement companies of 2020." We have been in business since 2002 helping people get relief from debt. We have an excellent track record and we keep our customer's best interest as our number one priority. We help settle your debts for substantially less than you currently owe, and we do all the heavy lifting while working to settle your accounts. We even work directly with your creditors so you don't have to deal with them at all.

The Better Business Bureau (BBB) trusts us and has awarded Pacific Debt with a BBB accreditation for debt relief. A BBB accredited rating means that Pacific Debt meets all the standards for quality, trustworthiness, and responsibility .

The BBB is not the only company that ranks us highly. US News and World Reports ranked Pacific Debt Inc. as one of The Best Debt Settlement Companies of 2020. You can learn about our rankings for yourself by reading our reviews. You can also read our accredited debt relief reviews from the Better Business Bureau website.

Trying to decide which company to trust for help with debt makes the decision all the more daunting.You may hear a lot of horror stories about debt consolidation companies. Pacific Debt is not a fly-by-night company. We have been in business since 2002 and have settled more than $300 million in debt for clients just like you.

Acknowledging that you have a lot of debt, or even multiple debts can be embarrassing. Our debt specialists understand how easy it is to get into debt and how difficult it is to get out. We are not here to judge you, we are here to help you.

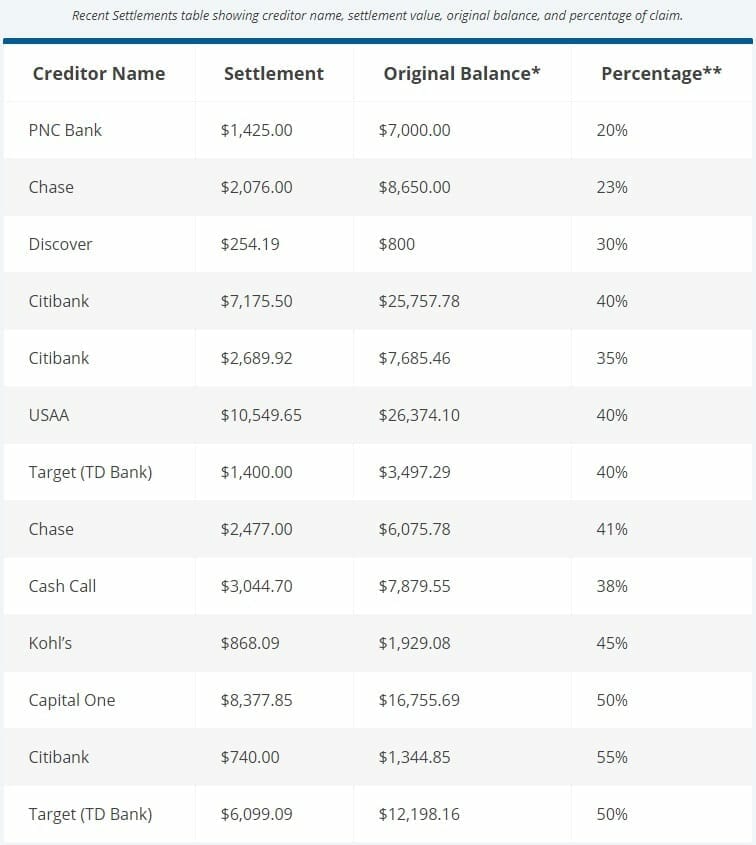

Debt Consolidation Companies BBB Accredited - Comparison Chart

The following table shows the companies that we work with, the average settlement and average original balances, plus the average decreased percentage that we have negotiated on behalf of clients just like you. Please note that these are not the only companies we work with, but they are a good representation.

How to Choose a Company for BBB Accredited Debt Consolidation Loans?

One of the best ways to choose from all the debt consolidation loan companies is to read real reviews from people who have been helped with our individualized debt relief program. That is why you can find verified reviews from real clients and links to independent rating sites like TrustPilot.

Always check the accreditation. Look for an A+ rating with the Better Business Bureau, membership with the International Association of Professional Debt Arbitrators. Check for good ratings with other independent rating companies.

And finally, give our debt specialists a call. You need to be comfortable with the person that you are speaking with and trust them to listen and understand your situation and explain all your options.

Get Started with Pacific Debt - One of the Best-Rated Debt Consolidation Companies BBB

When you are ready to become debt-free, we can help you just like our BBB accredited program has helped thousands of people. Since 2002, we’ve settled over $300 million in debt for our clients. We have probably already worked with your creditor. If you are looking for one of the best debt consolidation loan companies, contact us today to see how we can help.

We’ve included an informational video below to explain our services and what you can expect when you call Pacific Debt, Inc.

What debt can Pacific Debt Relief help with?

Debt consolidation can include unsecured debt like unsecured loans. Unsecured personal loans can include payday loans, credit card debt, medical expenses, and other unsecured debt. Most Americans have multiple debts including medical expenses, credit card debt, and student loans.

Unsecured loans are those that do not have an asset backing it. For instance, credit card debt is unsecured while a mortgage is a secured loan. While student loans are technically unsecured personal loans, they do not fall into the unsecured debt category that Pacific Debt can help with. However, one of our student loan partners may be able to help you.

Different Types of Debt Relief

There are four basic types of debt relief services available. Here is a breakdown of the four and their potential pros and cons.

Debt Consolidation

In debt consolidation, you roll all your high interest debts into one personal loan with a better interest rate. You then focus on paying off the personal loan. The main concern is finding a personal loan with a better interest rate. Since interest rates are based in part on your credit score, it may be difficult to find a loan with decent interest rates if you are in poor financial condition.

Debt consolidation loan rates must be lower than your existing debts in order for you to see any benefits. At present, personal loan rates range between 3% and 36%. The better your credit score the lower the interest rate you will be charged.

There may be minimum credit score requirements of 600 or 620 to usually get the best interest rates. If you can not meet that minimum credit score requirement, you may want to focus on improving your credit score until you reach the minimum credit score requirement or even achieve excellent credit scores.

Taking out a personal loan requires several years of regular monthly payments and usually do not have flexible repayment options. There is usually not a prepayment penalty, but make sure to always read the fine print.

Personal loans for debt consolidation

If you are considering debt consolidation, you first need to decide how much you need to pay off. Choose the highest interest debt and add it all up. You now know how much you need to apply for and what interest rates to look for.

Look for personal loans from credit unions, online personal loan lenders, secured loans like a home equity loan, and online lenders like P2P groups. Keep in mind that these debt consolidation lenders will charge origination fees and these origination fees decrease the amount available to repay your debts.

Secured personal loans for debt consolidation

Taking out a secured loan to repay your debts is usually problematic. A secured loan has something guaranteeing you will repay the loan. This is commonly your house (home equity loan). Because the loan is secured, interest rates are lowered than unsecured personal loans. However, if you fail to repay this loan funding source, you may lose your home or other guarantee.

Only take out secured loans if you have a concrete plan to repay the debt.

Credit card balance transfer

Besides taking out a personal loan, you may be able to use credit card debt consolidation. In this method, you may find zero balance transfer credit cards for consolidating credit card debt. You then can focus on making every monthly payment to pay off the zero balance transfer credit cards within the time limit. If you fail to pay off the consolidated debt within the time limit, the subsequent interest rates can be very high.

There is usually no prepayment penalty on balance transfer credit cards. Always make your monthly payment on time.

Debt Settlement

Settlement may be a great option and involves negotiating with your creditor to lower interest rates and/or total debt amount and thereby save money. Once the debt is negotiated, the creditor is usually then paid off. This settlement technique can be used in conjunction with a low interest rate personal loan. At Pacific Debt Relief, you save money into a savings account with monthly payments. The negotiated debt is paid through this savings account and means that you do not have to qualify for a personal loan.

This does not require a minimum credit score, but does require a minimum annual income that allows you to make a fixed monthly payment to your savings account. Debt Settlement does come with potential tax liability and credit score decreases. You should contact a legal tax expert for more information.

Get a free consultation today from our debt specialist.

Credit Counseling

Credit counseling involves learning how to better manage your finances and budget. You may be asked to develop a debt management plan that will help you repay your bills. It can include settlement and debt consolidation. You will also learn how to build a good credit score and credit report.

Credit counseling may be best for people who are just beginning to get into debt. However, even if you choose settlement or debt consolidation, credit counseling can help you stay out of debt in the future.

Bankruptcy

Bankruptcy is the last option to consider. Beside being expensive and time consuming, bankruptcy will most likely damage your credit and carries a social stigma. Always consult a bankruptcy specialist if you are contemplating this option.

FAQS

Pacific Debt Relief

750 B Street Suite 1700

San Diego, CA 92101

Hours of Operation

Mon-Thurs: 6am - 7pm PST

Friday: 6am - 4:30pm PST

Saturday: 7:30am - 4:30pm PST

Clients

Phone: (877) 722-3328

Fax: (619) 238-6709

Email: cs@pacificdebt.com

Non-Clients

Phone:

Fax: (619) 238-6709

Email: inquiries@pacificdebt.com

"Subscribe, follow, like, share, let's get social..."

"To eliminate debt one household at a time, while placing people first." - Pacific Debt

© 2024 Pacific Debt Inc. dba Pacific Debt Relief, all rights reserved.

California Privacy Policy |  Do Not Sell My Personal Information

Do Not Sell My Personal Information

GLBA Privacy Notice | CDRI Accredited Member

*We do not discriminate on the basis of race, color, religion, sex, marital status, national origin or ancestry.

*Please note that all calls with the company may be recorded or monitored for quality assurance and training purposes.

*Your visit to our website may be monitored and recorded from essential 3rd party scripts.

*Clients who make all their monthly program deposits pay approximately 50% of their enrolled balance before fees, or 65% to 85% including fees, over 24 to 48 months (some programs lengths can go higher). Not all clients are able to complete our program for various reasons, including their ability to save sufficient funds. Our estimates are based on prior results, which will vary depending on your specific circumstances. We do not guarantee that your debts will be resolved for a specific amount or percentage or within a specific period of time. We do not assume your debts, make monthly payments to creditors or provide tax, bankruptcy, accounting or legal advice or credit repair services. Pacific Debt is not a credit repair firm nor do we offer credit repair services. Our service is not available in all states and our fees may vary from state to state. Please contact a tax professional to discuss potential tax consequences of less than full balance debt resolution. Read and understand all program materials prior to enrollment. The use of debt settlement services will likely adversely affect your creditworthiness, may result in you being subject to collections or being sued by creditors or collectors and may increase the outstanding balances of your enrolled accounts due to the accrual of fees and interest. However, negotiated settlements we obtain on your behalf resolve the entire account, including all accrued fees and interest. C.P.D. Reg. No. T.S. 12-03825.