Get in touch

(833) 865-2028

inquiries@pacificdebt.com

Debt Relief Solutions

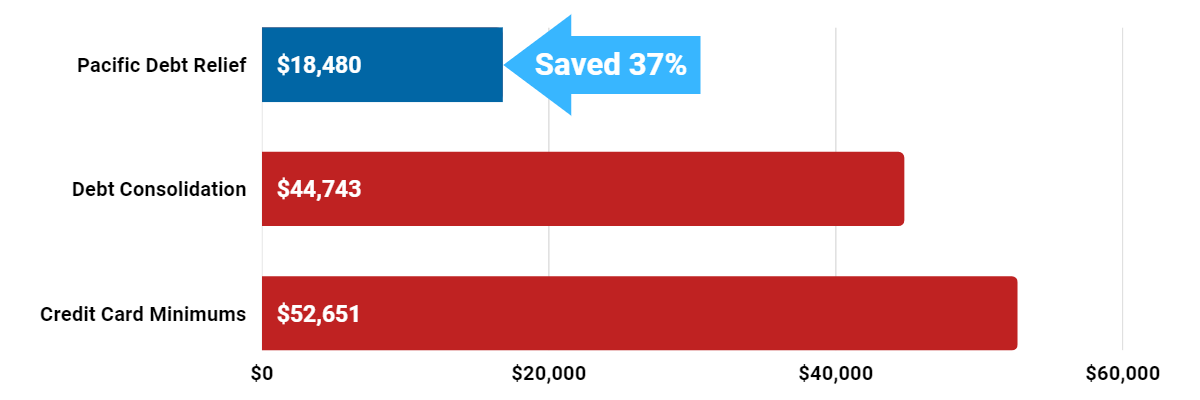

Reduce Your Credit Card Debt By Up To Half

Pacific Debt Relief offers a solution that can significantly reduce your debt to less than you currently owe. That means you could be debt-free in a fraction of the time it would take with other options.

Save thousands by lowering your debt balance and wiping away years of future interest and payments.

Get a

FREE consultation today with a debt specialist!

Debt Relief Solutions

Let's take a look at some debt relief options below to find out which of these debt solutions make the most sense for you. Click here if you'd rather speak to a debt specialist right away.

Consumer Credit Counseling

Consumer Credit Counseling (CCC) companies were first started by the credit card industry to provide debt relief to the enormous amount of people who began to fall delinquent on their payments. The majority of credit counselors and credit counseling agencies are paid a commission from your creditor based on how much debt they can recover from you and they may also charge a service fee.

In some cases, the debt help of a true nonprofit credit counseling agency and credit counselor may be helpful, as the interest rate reduction may be enough to alleviate the financial strain a consumer faces. Nonprofit credit counseling agencies also require you to learn how managing debt in the future will help you live debt free.

Debt Management Plans

A reputable credit counseling organization will help you set up a debt management plan. A debt management program is a way to roll all your payday loans and other unsecured debt into one payment. It is not a way to consolidate debt as there is no loan and it is not settlement because you still pay the full amount and full interest rates.

However, all too often the debt management plan's monthly payments required by a credit counseling organization can be too high for many to afford. The monthly payments can be as high, or higher, than the minimum payments a consumer was paying prior to enrollment with the consumer credit counselor. Once you start the program they will contact your creditors and enter you into a “Hardship Program” or debt management plan.

Bankruptcy / Consult an Attorney

Today, more than ever, people are filing personal bankruptcy as a way of getting away from the burden of their debt. Statistics show that the number one reason people are filing for bankruptcy is the harassment and pressure from companies trying to recover their money. For some people, bankruptcy is the only realistic options for debt relief.

The biggest benefit of bankruptcy is that this approach may provide immediate relief and can put an immediate stop to the harassment. In some cases, all of your unsecured debt is forgiven and you can get a “clean slate”.

New laws were passed that make it considerably harder and less desirable to file for bankruptcy as a way out. With this in mind, even if you are able to file for bankruptcy, there is a good chance you will still have to pay some or all of your debts over a period of time. On the plus side, bankruptcy does offer some financial protection for your home and some income.

To determine what type of bankruptcy you may qualify for we strongly encourage you to speak with an attorney in your state. Only a licensed attorney in your state can review what debt help is available to you through bankruptcy.

Negative Effects of Bankruptcy

The negative aspect to consider with bankruptcy is the effect on one's credit history. Bankruptcy can ruin your financial life for many years to come. The bottom line is that it may stay on your credit report for up to 10 years. In addition, you'll pay immensely for those important purchases that you make later on in life.

For example, if you want to purchase a house in the future, the interest rate will be much higher than for the average consumer who never has filed bankruptcy. In addition, bankruptcy may be taken into account when applying for a job, an insurance policy, applying for a car loan, filling out a renter's application, etc.

As you can see, bankruptcy isn't as appealing as it may first appear, although in some circumstances it is the best, if not only, solution. Only a licensed attorney may provide debt help guidance as to whether bankruptcy is a suitable option for you.

Debt Consolidation Loans / Credit Card Debt Consolidation

When falling victim to financial problems, debt consolidation loans are one of the most common debt solutions people think of for credit card debt consolidation. In some instances, this option may be a good fit for you if you have excellent credit and can obtain a personal loan with a much lower interest rate and a manageable monthly payment. However, many people who choose to go this route may find themselves in much deeper financial trouble then they were to begin with.

Most consolidation loans issued through a financial institution are secured by collateral, such as your house, car or other personal property. By obtaining this type of loan all you are really doing is exchanging an unsecured debt for a secured debt that you will still need to pay interest on. Another downside is that it may put your assets in an accessible position for the loan company to go after in the event of default. In this case, all the leverage shifts over to the creditor.

This option can make sense if you can obtain a new credit card debt consolidation loan with a much lower interest rate and a payment the comfortably fits within your budget.

Only making the minimum payments

Unfortunately, if you are struggling to meet your monthly payments, just making the minimums or behind on your payments, you may be in a situation where your debt will take many years to pay off — if at all. By simply paying the minimum each and every month, as much as 85% of your payments are going to interest and it may take you 25 years or more to pay off your debt in full!

In the long run, paying the minimum is not a solution to your financial situation. Consumers should consider factors such as expected future income as well possible budget changes when determining whether it makes sense to try and pay off credit cards on their own versus other debt solutions such as debt settlement or bankruptcy.

For instance, if a consumer is expecting to be making more money in the near future, or has simply had a temporary financial setback, continuing that minimum payment might make sense. Conversely, if someone is on a fixed income and has analyzed their budget, continuing to pay minimum amounts on debt payments may not make sense and other debt solutions such as debt settlement, credit counseling or bankruptcy may be appropriate.

Consumers may also wish to contact their creditors directly and attempt to negotiate lower interest rates or payment terms on their own prior to seeking other debt relief options. Some creditors will offer short-term hardship programs or lower payment terms. In many cases, creditors will not offer debt help unless the consumer is already past due.

Debt Settlement with Pacific Debt Relief

Debt settlement maybe your best option to reduce your debt substantially. In a debt settlement program, the debt settlement company negotiates with creditors and debt collectors to lower the interest rate and the total amount owed. While you can do this on your own, a debt settlement company knows which creditors are more likely to settle. Our debt settlement programs work with most major credit card companies and have developed an excellent reputation for settling unsecured debt.

Most debt settlement companies deal only in unsecured debt like credit card bills, medical bills, and personal loans. While debt settlement is not for everyone, it can drastically turn around your financial situation.

Pacific Debt Relief is a national debt settlement company that has settled over $300 million in debt since 2002. If you are eligible for our debt relief solution and follow through with the requirements, you can be debt free within two to four years.

Get a free consultation today!

Eligibility

To be eligible for the Pacific Debt Relief program, you must:

- Enrolled debt of at least $10,000 in unsecured debts (credit card debt, payday loans, personal loans, previous consolidation loans, medical bills, collections and repossessions, business debts, and some student loans). Can be from multiple debts.

- Difficulties making payments and late fees.

- We offer national debt relief, but you must live in a state where Pacific Debt operates. Pacific Debt offers services in the following states:

Alabama, Alaska, Arizona, Arkansas, California, Colorado, District of Columbia, Florida, Idaho, Indiana, Kentucky, Louisiana, Massachusetts, Maryland, Michigan, Missouri, Mississippi, Montana, North Carolina, Nebraska, Nevada, New Mexico, New York, Oklahoma, Pennsylvania, South Dakota, Texas, Utah, Virginia, Wisconsin - * Since not all states are included, not all clients can enroll in our company. People in other states can be connected to one of our trusted debt relief companies

Call for a free consultation today!

Debt Relief Accreditation

Pacific Debt Relief is accredited by:

- The Consumer Debt Relief Initiative

- International Association of Professional Debt Arbitrators

- Better Business Bureau A+ Rating with over 800 reviews

Like all debt relief companies, we are under the oversight of the Federal Trade Commission.

How Debt Settlement Works

We begin negotiating with your creditors to lower interest and total debt. You make regular payments, based on your budget, to a dedicated savings account. After you build up enough savings, Pacific Debt pays off each creditor.

We do not charge upfront fees - only non-reputable debt settlement companies charge upfront fees! We do charge a fee of 15-25% of the total debt enrolled as we achieve results. During your time with Pacific Debt, you will receive personal attention from your personal account manager and certified debt specialist.

Get a free consultation today!

Debt Settlement Concerns

There may be some drawbacks to debt settlement. First, because you will most likely will need to stop paying bills to convince creditors or debt collectors that you are serious, your credit scores can take some damage. The second issue is that debt settlement can come with tax debt as the IRS sees debt forgiveness as income.

To avoid too much of an effect from debt forgiveness, we recommend you speak with a qualified tax advisor.

Read Customer Reviews from Pacific Debt Relief

If you search other debt settlement companies, always read the reviews from real customers about their debt settlement programs. Read what real clients say about Pacific Debt's debt relief services from reading our reviews.

With ratings and reviews like these, it is no wonder that we are a top debt relief company. Pacific Debt has helped thousands of people reduce their debt and find debt relief. Since 2002, we've settled over $300 million in debt for our clients.

Check out our success stories from satisfied clients in San Francisco. Hear from our satisfied clients in Philadelphia. See how we've transformed the financial lives of our clients in Arlington.

Our debt settlement program is designed for those consumers facing financial hardship who value getting out of debt over maintaining their credit score. We also have a strong presence in many large cities such as Tampa, helping many clients settle their debts. Read about our success stories from Austin.

Pacific Debt Relief is one of the top-rated debt relief companies in San Diego. See how we've made a difference for our clients in Yonkers. Our debt relief program also operates throughout the United States.

Read about how we've helped individuals in Orlando achieve financial freedom. We've also received positive feedback from our clients in New York. Discover the experiences of our clients from Pennsylvania.

Contact us today to see how we can help you understand your debt relief solutions and help you eliminate your debt.

*Disclaimer: Pacific Debt Relief explicitly states that it is not a credit repair organization, and its program does not aim to improve individuals' credit scores. The information provided here is intended solely for educational purposes, aiding consumers in making informed decisions regarding credit and debt matters. The content does not constitute legal or financial advice. Pacific Debt Relief strongly advises individuals to seek the counsel of qualified professionals before undertaking any legal or financial actions.

Ready to get started?

Pacific Debt Relief

750 B Street Suite 1700

San Diego, CA 92101

Hours of Operation

Mon-Thurs: 6am - 7pm PST

Friday: 6am - 4:30pm PST

Saturday: 7:30am - 4:30pm PST

Clients

Phone: (877) 722-3328

Fax: (619) 238-6709

Email: cs@pacificdebt.com

Non-Clients

Phone:

Fax: (619) 238-6709

Email: inquiries@pacificdebt.com

"Subscribe, follow, like, share, let's get social..."

"To eliminate debt one household at a time, while placing people first." - Pacific Debt

© 2024 Pacific Debt Inc. dba Pacific Debt Relief, all rights reserved.

California Privacy Policy |  Do Not Sell My Personal Information

Do Not Sell My Personal Information

GLBA Privacy Notice | CDRI Accredited Member

*We do not discriminate on the basis of race, color, religion, sex, marital status, national origin or ancestry.

*Please note that all calls with the company may be recorded or monitored for quality assurance and training purposes.

*Your visit to our website may be monitored and recorded from essential 3rd party scripts.

*Clients who make all their monthly program deposits pay approximately 50% of their enrolled balance before fees, or 65% to 85% including fees, over 24 to 48 months (some programs lengths can go higher). Not all clients are able to complete our program for various reasons, including their ability to save sufficient funds. Our estimates are based on prior results, which will vary depending on your specific circumstances. We do not guarantee that your debts will be resolved for a specific amount or percentage or within a specific period of time. We do not assume your debts, make monthly payments to creditors or provide tax, bankruptcy, accounting or legal advice or credit repair services. Pacific Debt is not a credit repair firm nor do we offer credit repair services. Our service is not available in all states and our fees may vary from state to state. Please contact a tax professional to discuss potential tax consequences of less than full balance debt resolution. Read and understand all program materials prior to enrollment. The use of debt settlement services will likely adversely affect your creditworthiness, may result in you being subject to collections or being sued by creditors or collectors and may increase the outstanding balances of your enrolled accounts due to the accrual of fees and interest. However, negotiated settlements we obtain on your behalf resolve the entire account, including all accrued fees and interest. C.P.D. Reg. No. T.S. 12-03825.